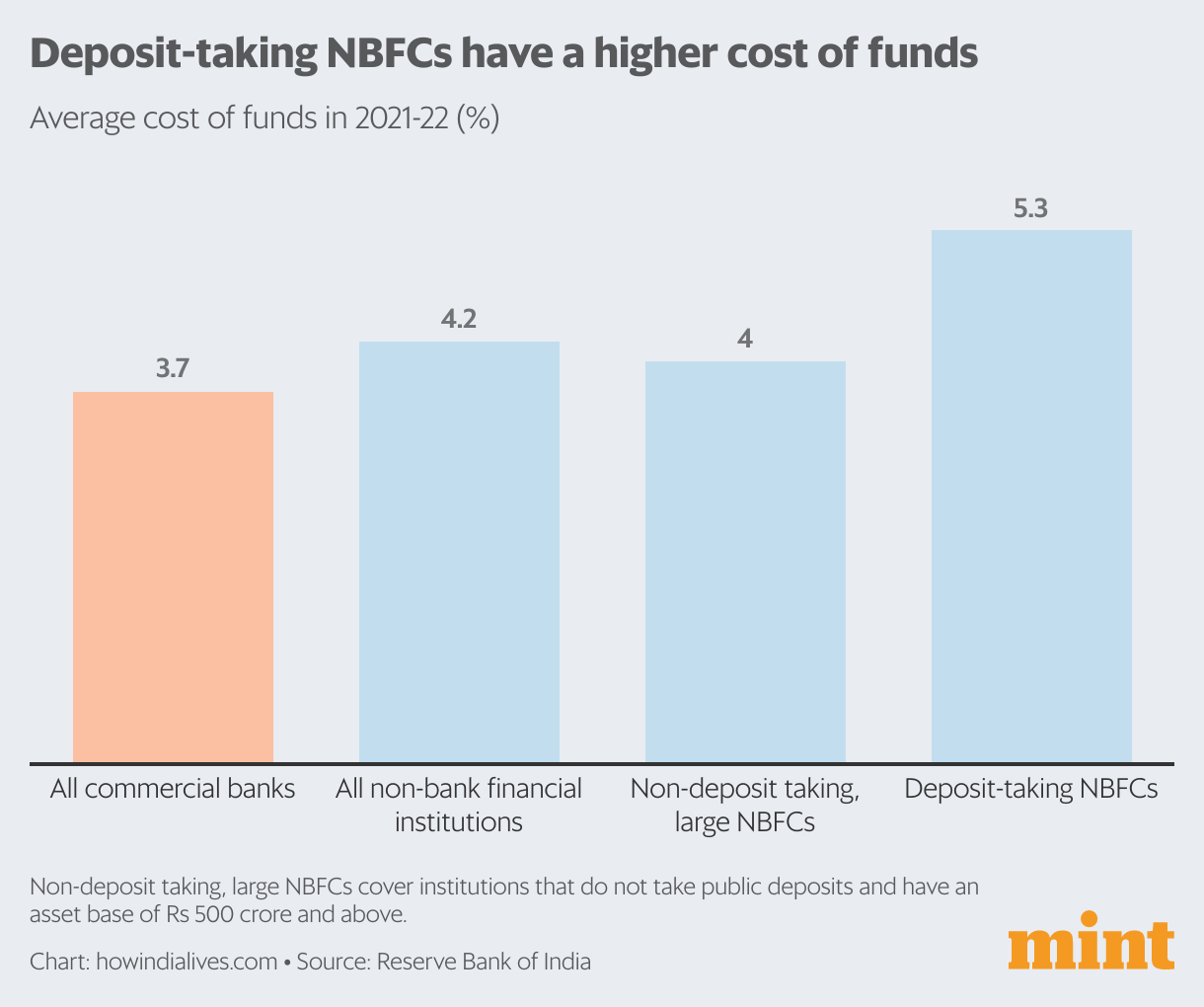

A significant cause for the long-awaited merger of HDFC and HDFC Financial institution was prices. Within the Indian monetary system, solely banks can increase funds from the general public by present accounts and financial savings accounts, on which they pay both no or very low curiosity. Such deposits accounted for 44% of HDFC Financial institution’s fund base in 2022-23. In distinction, non-bank monetary corporations (NBFCs) such because the erstwhile HDFC can solely increase time period deposits from the general public, that too sometimes at increased rates of interest than banks. Thus, the common value of funds for HDFC was a lot increased than that for HDFC Financial institution.

But, this relative drawback on value of funds alone doesn’t dismiss a case to be an NBFC. The NBFC sector, as an entire, is diversified when it comes to measurement, possession and enterprise profile. Broadly, NBFCs are labeled into these which might be allowed to boost deposits from the general public (like HDFC) and people that aren’t.

The Reserve Financial institution of India, which regulates NBFCs, additional splits the second class into establishments whose asset base exceeds ₹500 crore, which it considers ‘systemically vital’. This class contains a number of giant government-backed corporations (similar to Energy Finance Company), which account for 45% of property on this class. Their government-owned standing means they’ll increase funds at a decrease value, thus flattening the price of funds for the NBFC sector as an entire. In distinction, NBFCs allowed to boost public deposits account for 14% of the sector and their value of funds is often increased than that of banks.

Margin enhance

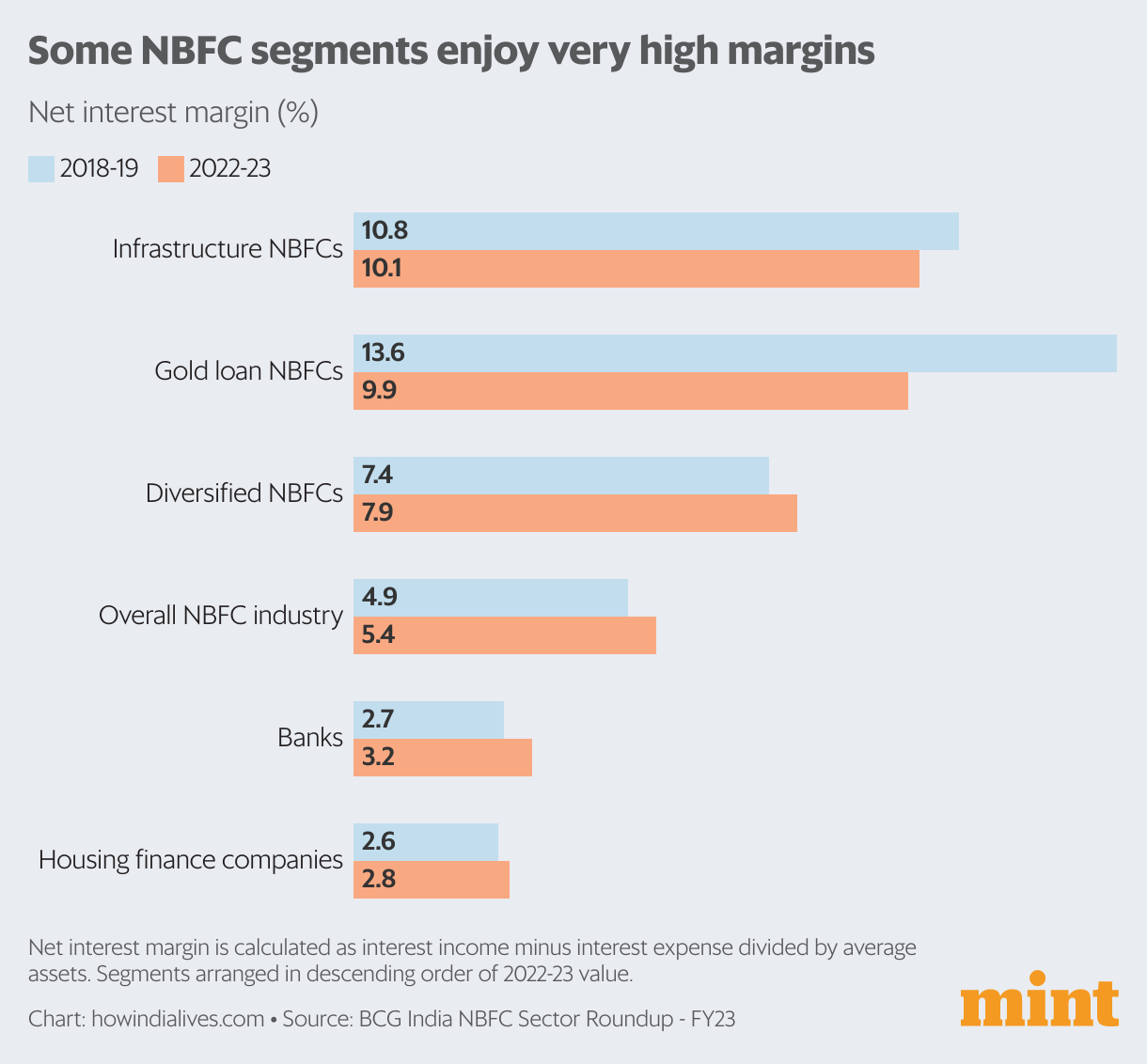

The enterprise case for NBFCs comes from margins. As an entire, margins of NBFCs are typically a lot increased than that of banks. It is because NBFCs are extra centered on higher-margin retail loans similar to gold loans, automobile loans and microfinance. Whereas the share of retail loans in whole loans for each teams is roughly the identical (round 28% in 2022-23), banks are inclined to have a a lot bigger share of lower-margin dwelling loans of their mortgage guide. Excluding dwelling loans, the share of retail loans in total loans for NBFCs was 27.7% versus 13.8% for banks.

Thus, as an entire, the online curiosity margin for NBFCs was 2.2 share factors increased than for banks in 2022-23. Amongst NBFC segments, infrastructure mortgage and gold mortgage corporations had the best margins. The exceptions within the NBFC sector have been housing finance corporations, the class to which HDFC belonged. Because of intense competitors from banks, margins for housing finance establishments have been decrease than for banks.

Market approval

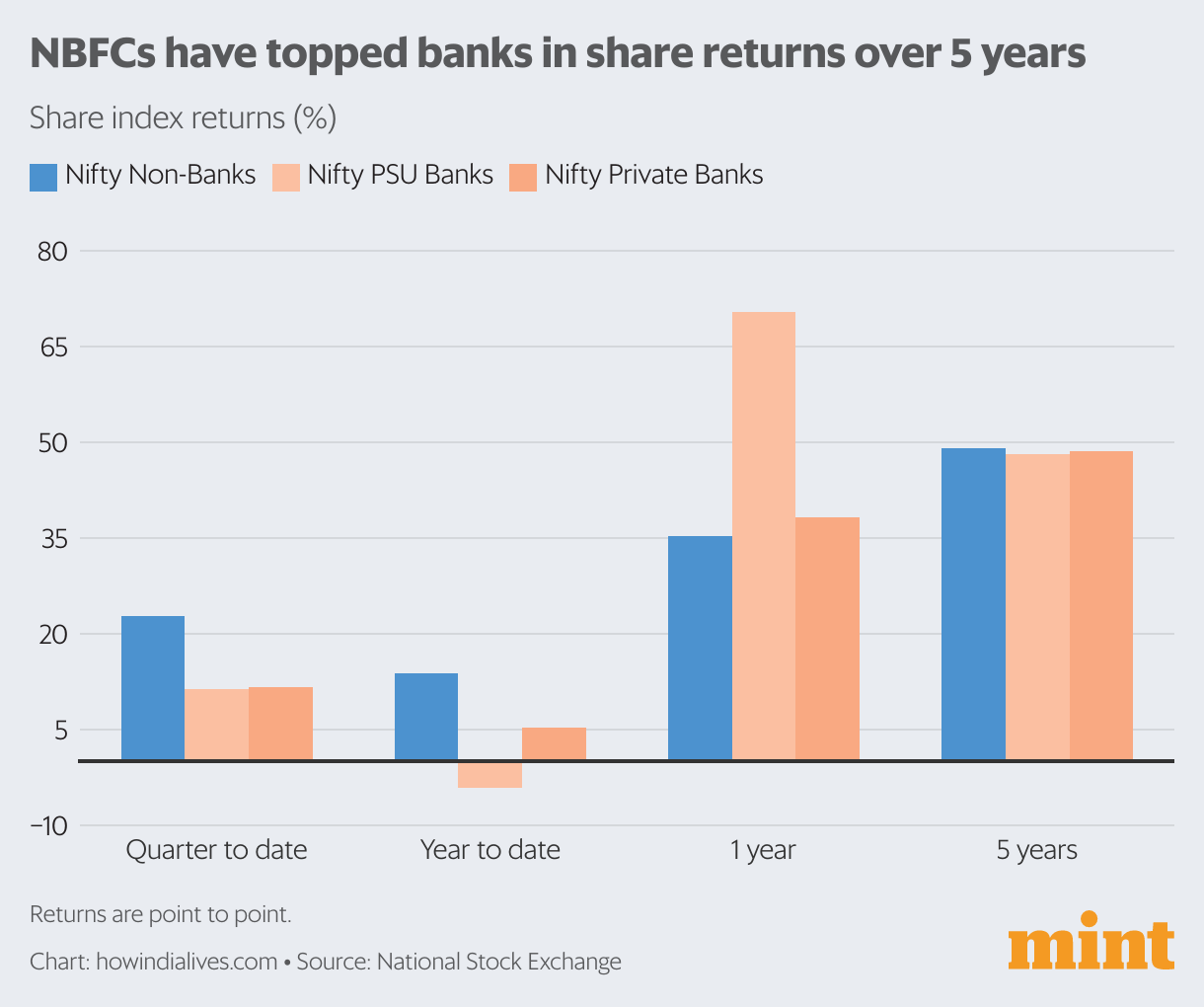

NBFCs which might be extra retail-oriented, particularly in higher-margin segments, have carried out nicely on the expansion entrance previously few years. Thus, over a five-year interval, share efficiency of the NBFC set has topped each non-public banks and public sector banks. Over a one-year interval, whereas inventory market efficiency for the monetary sector as an entire has been robust, NBFCs have trailed banks, particularly public sector banks, whose shares have been on a tear until the final quarter.

Valuations of enormous NBFCs similar to Bajaj Finance and Cholamandalam Finance prime even that for main banks. In accordance with a assessment of the NBFC sector by the Boston Consulting Group, as of end-Might, Bajaj and Cholamandalam had a price-to-book ratio of 8.2 and 6, respectively. By comparability, it was 3.2 for HDFC Financial institution, 3.6 for the erstwhile HDFC and 1.7 for SBI. In accordance with BCG, the so-called ‘diversified’ NBFCs, who’re lively in a number of sectors, commanded increased valuations.

Residence-loan hurdle

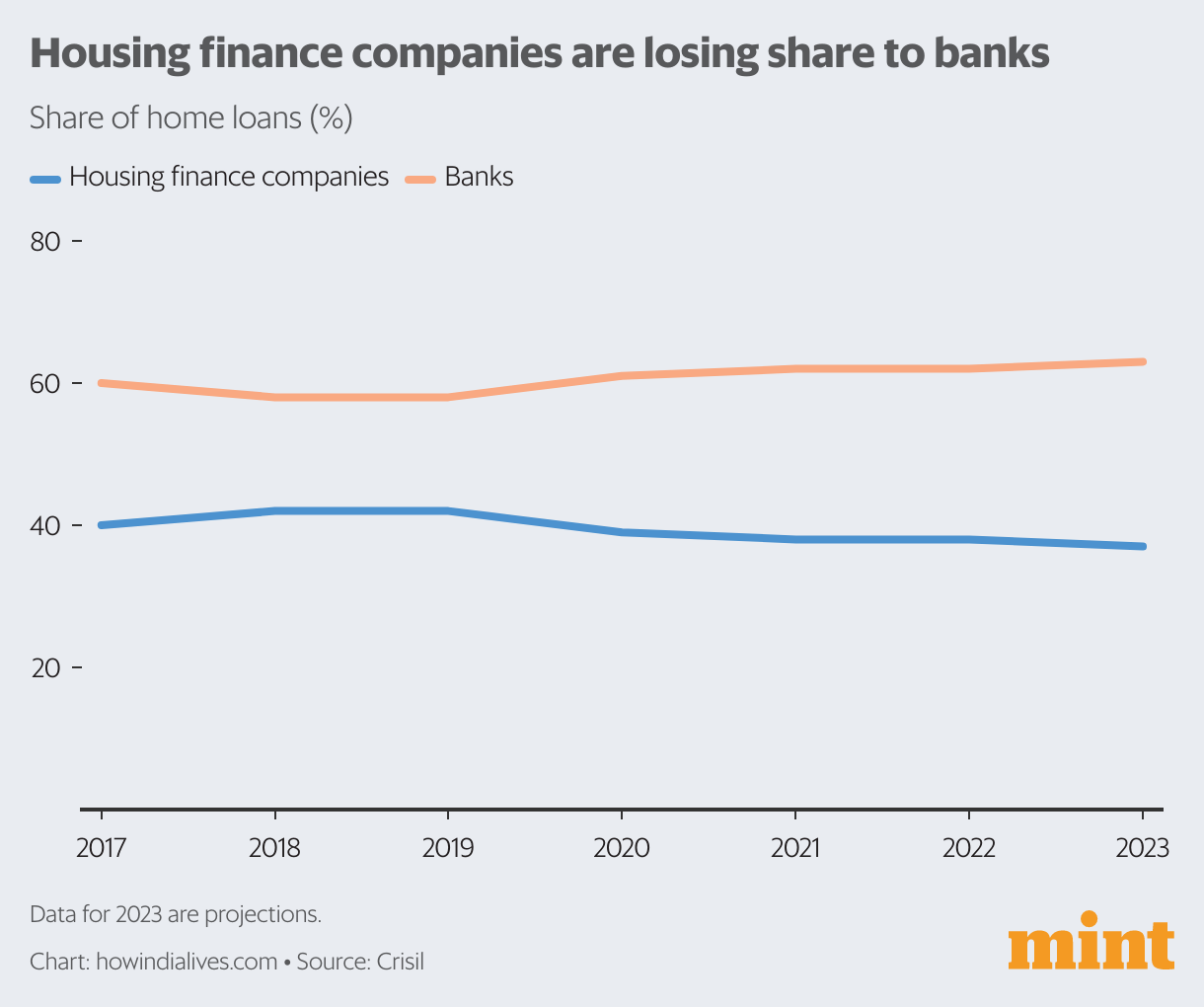

The HDFC merger additionally places the highlight on housing finance corporations (HFCs). Given the extreme competitors from banks and low margins in housing finance, do HFCs have a future? Whereas the post-covid restoration led to robust home-loan progress for NBFCs lively within the sector, a Crisil report final 12 months argued that HFCs have been anticipated to proceed dropping home-loan market share to banks amid stiff competitors. “Whereas entry to funding shouldn’t be a giant problem for many HFCs, aggressive borrowing value is essential versus banks, which profit from low-cost deposit funding,” the report stated.

Between 2019 and 2022,HFCs have misplaced 4 share factors of market share to banks, who now account for 62% of the home-loan market. “This pattern is unlikely to reverse within the close to time period,” Crisil notes. Whereas NBFCs oriented round dwelling loans can be challenged, the enterprise case for the extra diversified NBFCs stays.

www.howindialives.com is a database and search engine for public information

Supply: Live Mint