Punctuating that sterling efficiency is a tenet of investing that Munger and Buffett embraced, articulated and, most significantly, put into observe at Berkshire for about six many years. That tenet was ‘worth investing’, and it rested on a set of foundational ideas.

In Worth We Belief

One, purchase into companies, not into firms. Two, purchase good companies at good costs. Three, good companies construct a aggressive moat round them, be it by utility, branding, buyer stickiness, or regulatory assemble. 4, don’t purchase a enterprise you don’t perceive, and that’s why Berkshire has not often purchased a know-how enterprise despite residing by three many years of a digitalizing world. 5, apart from development, emphasize on money flows and profitability whereas assessing a enterprise. Six, don’t overpay for a enterprise. Seven, give it time. Eight, ignore the inventory market. 9, empower your chief government officers (CEOs).

It was easy, unglamorous, silent, slip-under-the-radar stuff. And it delivered returns that have been method superior to the noisy, moody, hyperactive inventory market that pulls traders to it, and makes them dance to its tune.

Yearly, Buffett sends out a letter to shareholders that outlines Berkshire’s efficiency within the final yr, or dives deep into an organization’s efficiency, or owns as much as errors, or nudges shareholders to the annual Berkshire retreat. It’s a simple learn stripped of jargon, backslapping and pontificating. A phrase cloud of the highest 75 operative phrases that appeared in 45 annual letters between 1977 and 2022 underscore how enshrined worth investing and first ideas have been at Berkshire Hathaway.

View Full Picture

View Full Picture

Making of a Conglomerate

Initially, Berkshire Hathaway was neither an funding firm nor a conglomerate. It was a textile firm in hassle that Buffett purchased 7% of in 1964, with the purpose of cashing in on an exit. He ended up staying on and purchased extra. He step by step began realizing his imaginative and prescient of turning it right into a holding firm, whilst Charlie Munger joined him, an ready foil. “The blueprint he (Munger) gave me was easy: Neglect what about shopping for honest companies at great costs; as an alternative, purchase great companies at honest costs,” wrote Buffett famously in a 2014 notice when Berkshire turned 50.

Berkshire moved on two tracks. The primary was as a holding firm, whereby it purchased companies, often 100%, and gave full autonomy to their CEOs. The second was as an funding firm, whereby it invested in listed shares.

In 1980, Berkshire had about $1 billion in belongings. Of this, about $525 million, or roughly half, was in shares, and the remaining was a part of the companies run by it. These firms have been principally in six sectors: insurance coverage, textiles, retailing, sweet, promotional companies and newspapers.

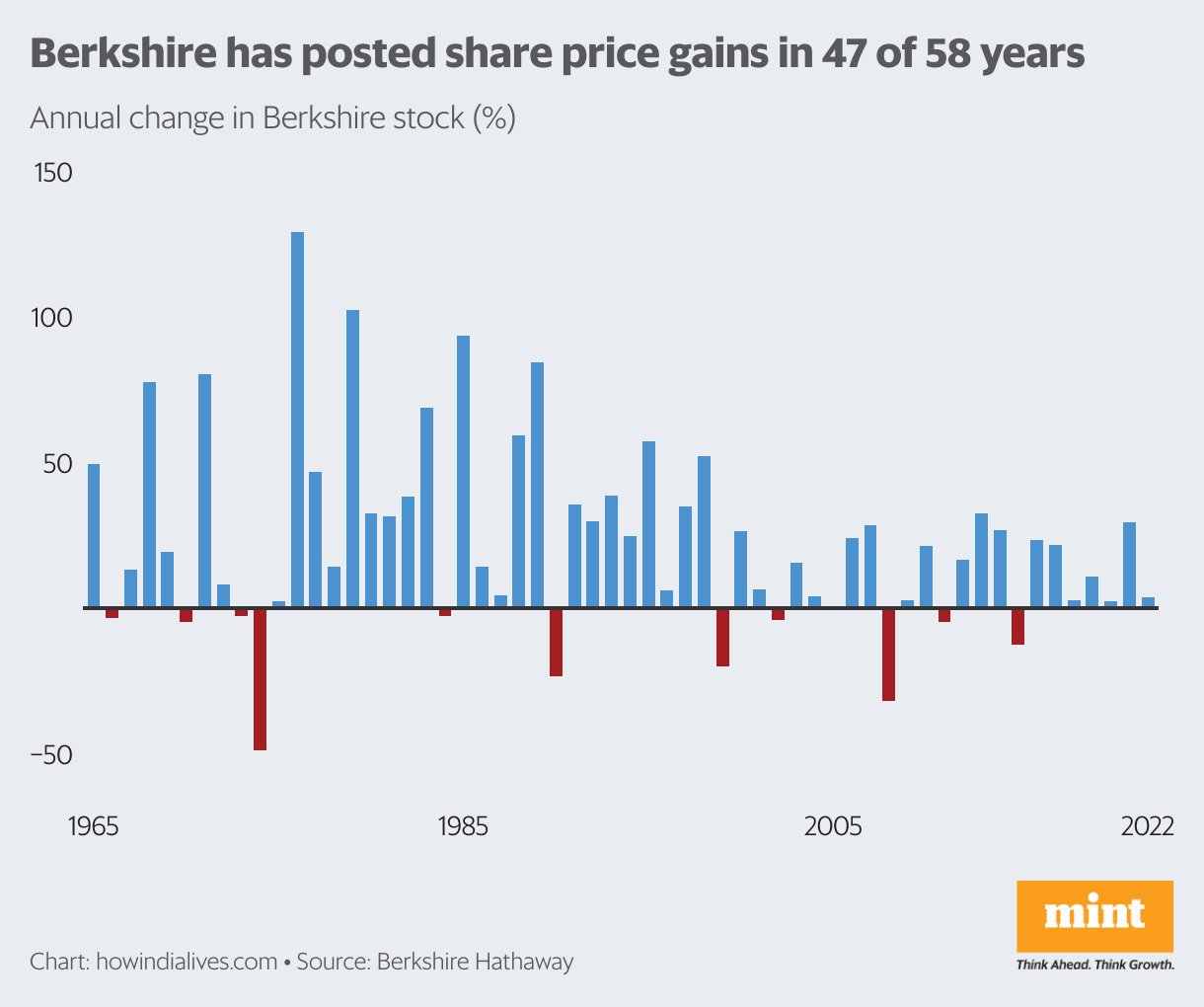

In 2022, Berkshire’s belongings stood at about $948 billion—a compounded annual development of 17%. Of this, about $308 billion, or about 30%, was in listed companies run by others. The remainder was housed in companies owned by it. Berkshire is now a sprawling conglomerate of about 70 firms throughout a number of sectors, with additions together with rail transport, energy, pure gasoline, attire, aviation companies and quick meals. In all this whereas, regardless of being oblivious to the market, Berkshire has had a constructive return in 47 of the 58 years since 1965.

Again Them—Huge

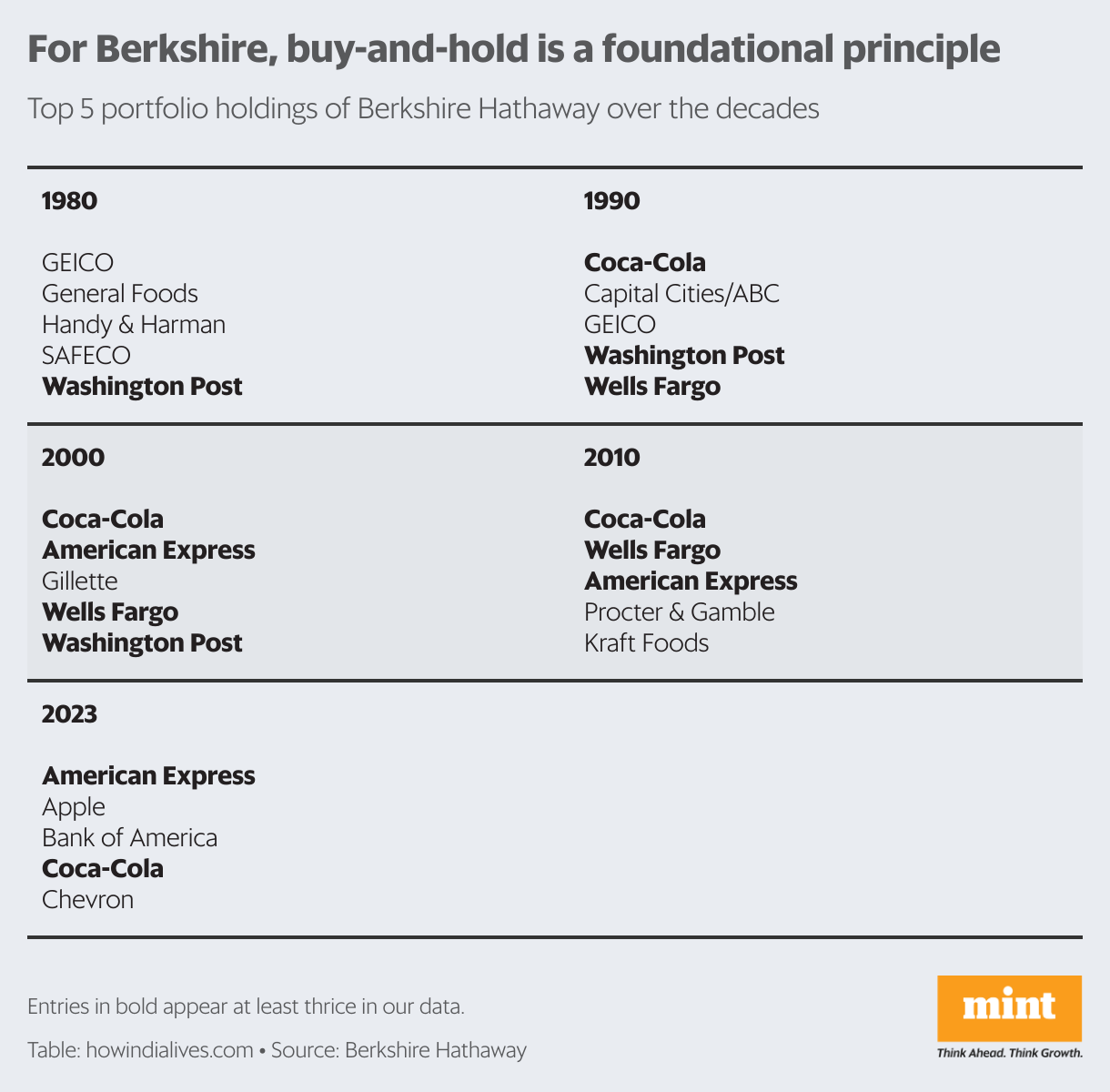

An enormous cause for that is the Buffett-Munger partnership, and the way they married elementary ideas of investing with execution. They deliberated on purchase choices. However as soon as they selected a enterprise, they dedicated in a giant method—and for the lengthy haul. For instance, the highest 5 holdings within the Berkshire inventory portfolio frequently account for 60% of its complete worth, much more. It’s held on to companies like Coca-Cola and American Categorical for 30-40 years.

Buffett was effusive in his reward for Munger. In his letter marking Berkshire at 50, he wrote: “…Charlie has a wide-ranging brilliance, a prodigious reminiscence, and a few agency opinions. I’m not precisely wishy-washy myself, and we generally don’t agree. In 56 years, nevertheless, we’ve by no means had an argument. After we differ, Charlie often ends the dialog by saying: ‘Warren, assume it over and also you’ll agree with me since you’re sensible and I’m proper.’” They have been sensible and proper—an terrible lot.

www.howindialives.com is a database and search engine for public information

Supply: Live Mint