A little bit over every week after itemizing, Paytm’s father or mother One97 Communications introduced its outcomes for Q2FY22. The corporate’s income from operations rose 64%, whereas consolidated internet loss widened 8% to Rs 473 crore. A key drive of the expansion in income was the 52% development in non-UPI volumes. In an interview to TOI, Vijay Shekhar Sharma, the corporate’s founder & CEO explains how the losses aren’t brought on by burning cash for volumes however by conservative accounting, which supplies for acquisition prices upfront.

You may have introduced your outcomes inside days of itemizing. What has been the analyst response?

We had our first earnings name. I can solely reference the expertise with what I’m conversant in. I’d examine it to the expertise of becoming a member of an engineering school after coming from Aligarh to Delhi. The IPO course of was like getting admission and the earnings name was the examination instantly after. Earlier than the decision, the three of us who had been on the decision threw questions at one another.

Your contribution margin has jumped however the loss has additionally elevated? Additionally many lay traders don’t perceive contribution margin.

Our margins have grown sooner than our revenues. Even when folks don’t perceive contributory income, which now we have tried to clarify, the ebitda (earnings earlier than curiosity, taxes, depreciation, and amortisation) is an easy measure. Our ebitda margins are a lot larger. We used to have an ebitda margin of -64%, which is now -39%.

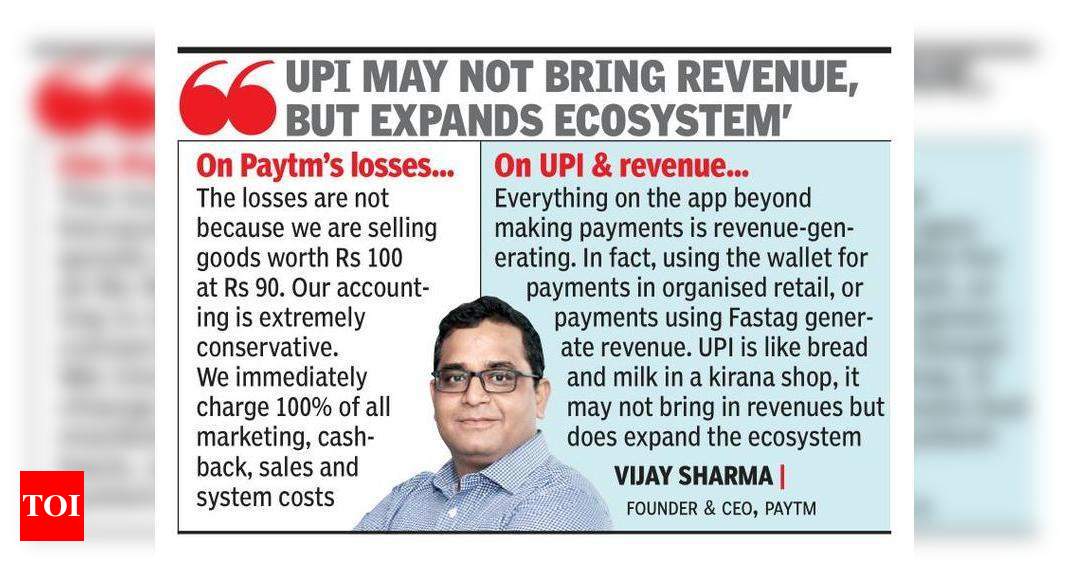

What’s the motive for the rise in prices?

As a enterprise, our bills can broadly be categorised into folks and advertising and marketing. Our advertising and marketing bills are flat however we’re hiring extra folks, extra engineers, which is sweet. That is the equal of rising a manufacturing facility in a producing enterprise. The distinction between investing in a manufacturing facility and our funding is that we don’t amortise our acquisition prices. A service provider we purchase is a subscriber for no less than one 12 months they usually present income both by way of lending or MDR over the 12 months whereas the buying value is offered upfront. The losses aren’t as a result of we’re promoting items price Rs 100 at Rs 90. Our accounting is extraordinarily conservative. We instantly cost 100% of all advertising and marketing, cashback, gross sales and system prices. The explanation why ebitda has improved is that retailers acquired earlier are producing income.

Lots of analyst focus seems to be on the lending enterprise…

Banks have the bottom value of funds they usually even have an obligation to increase precedence sector loans with a worth of under Rs 50,000. We’ve a expertise platform that may ship, service and acquire loans. These are short-term loans and now we have demonstrated {our capability} by way of a few cycles and the pandemic. Our common ticket dimension is Rs 4,000, which no lender couldn’t contact. It’s the best factor to increase a Rs 1,000-crore mortgage by way of a single company relationship. We’re disbursing Rs 7,500 crore (a billion {dollars}) by way of small loans.

How do you generate income on funds with zero charges on UPI?

I’ve at all times maintained that it is very important have zero charges on UPI because it helps to create a digital acceptance ecosystem. Paytm makes income as a result of as soon as a retail service provider matures, they begin accepting different digital fee devices as effectively. Our non-UPI has grown 52%. On non-UPI transactions, we earn extra as we additionally get issuer charges. Our transaction processing value as a share of volumes has gone up. As a share of gross merchandise worth, fee processing prices have come down.

The shopper base you talked about (5 crore+) is greater than the inhabitants of South Korea. Why is Paytm Mall not utilized by high manufacturers for presents?

WalMart has a enterprise mannequin of ‘on daily basis low value’. We comply with an analogous technique in funds. Fairly than providing offers in just a few high-end manufacturers, we provide cashback on each transaction whether or not it’s petrol, electrical energy or an iPhone. Our focus isn’t on choose anchor clients and the mannequin is extra inclusive. Additionally, in contrast to e-commerce platforms, we don’t promote our merchandise, quite we’re open to internet hosting all e-commerce platforms on our app.

Some analysts are of the view that funds can’t be a moat…

Fee apps can both come from banks or unbiased service suppliers. It’s now clear that fee app corporations work more durable than banks in offering a buyer expertise. Now if one is utilizing a fee app for transactions, it’s logical that clients will desire these apps the place their cash is. Banks can retailer cash, however they don’t present the identical fee expertise. Paytm has the benefit of storing cash in both the checking account, pockets or by way of a credit score facility. We’ve introduced innovation within the methodology of fee (QR code, cellphone quantity) and added the following degree of comfort (soundbox). Clients can use their fastened deposits to make funds seamlessly. Clients can use Paytm for toll fee on Fastag with out blocking their funds.

So apart from lending, how will Paytm be getting cash?

Every thing on the app past making fee is income producing. Actually utilizing the pockets for funds in organised retail, or funds utilizing Fastag generates income. UPI is like bread and milk in a kirana store, it might not herald revenues however does develop the ecosystem.

Fee gateway Billdesk made a revenue of Rs 270 crore. How a lot did Paytm make within the fee gateway enterprise?

Our income from fee providers to retailers was up 64% to Rs 400 crore. That is pushed by non-UPI fee quantity development in fee gateway and development in units.

The RBI has mentioned {that a} fee financial institution’s transition to a small finance financial institution will be allowed solely after 5 years?

We’re lower than one 12 months away from finishing 5 years (om Might 2022) and are open to exploring the alternatives ought to they come up. Additionally, Paytm Funds Financial institution’s internet price is Rs 400 crore as in opposition to the Rs 300 crore prescribed by the regulation.

The pandemic and subsequent lockdowns gave a push to digital fee and e-commerce. What affect would the easing of restrictions have?

There’s an upside to income from journey, film and occasion ticketing, which had been hit by lockdown in the course of the pandemic. We predict an excellent response from clients because the unlockdown takes place.

How do you count on the market to reply?

Hopefully extra folks available in the market are capable of see our efficiency intimately. We listed in India so that everybody will get a possibility to take part. It is vital that the retail investor will get the entire image. Sure, our losses have elevated 8%, however our revenues have gone up 64% and ebitda has gone up 50%. That’s the full image.

You may have introduced your outcomes inside days of itemizing. What has been the analyst response?

We had our first earnings name. I can solely reference the expertise with what I’m conversant in. I’d examine it to the expertise of becoming a member of an engineering school after coming from Aligarh to Delhi. The IPO course of was like getting admission and the earnings name was the examination instantly after. Earlier than the decision, the three of us who had been on the decision threw questions at one another.

Your contribution margin has jumped however the loss has additionally elevated? Additionally many lay traders don’t perceive contribution margin.

Our margins have grown sooner than our revenues. Even when folks don’t perceive contributory income, which now we have tried to clarify, the ebitda (earnings earlier than curiosity, taxes, depreciation, and amortisation) is an easy measure. Our ebitda margins are a lot larger. We used to have an ebitda margin of -64%, which is now -39%.

What’s the motive for the rise in prices?

As a enterprise, our bills can broadly be categorised into folks and advertising and marketing. Our advertising and marketing bills are flat however we’re hiring extra folks, extra engineers, which is sweet. That is the equal of rising a manufacturing facility in a producing enterprise. The distinction between investing in a manufacturing facility and our funding is that we don’t amortise our acquisition prices. A service provider we purchase is a subscriber for no less than one 12 months they usually present income both by way of lending or MDR over the 12 months whereas the buying value is offered upfront. The losses aren’t as a result of we’re promoting items price Rs 100 at Rs 90. Our accounting is extraordinarily conservative. We instantly cost 100% of all advertising and marketing, cashback, gross sales and system prices. The explanation why ebitda has improved is that retailers acquired earlier are producing income.

Lots of analyst focus seems to be on the lending enterprise…

Banks have the bottom value of funds they usually even have an obligation to increase precedence sector loans with a worth of under Rs 50,000. We’ve a expertise platform that may ship, service and acquire loans. These are short-term loans and now we have demonstrated {our capability} by way of a few cycles and the pandemic. Our common ticket dimension is Rs 4,000, which no lender couldn’t contact. It’s the best factor to increase a Rs 1,000-crore mortgage by way of a single company relationship. We’re disbursing Rs 7,500 crore (a billion {dollars}) by way of small loans.

How do you generate income on funds with zero charges on UPI?

I’ve at all times maintained that it is very important have zero charges on UPI because it helps to create a digital acceptance ecosystem. Paytm makes income as a result of as soon as a retail service provider matures, they begin accepting different digital fee devices as effectively. Our non-UPI has grown 52%. On non-UPI transactions, we earn extra as we additionally get issuer charges. Our transaction processing value as a share of volumes has gone up. As a share of gross merchandise worth, fee processing prices have come down.

The shopper base you talked about (5 crore+) is greater than the inhabitants of South Korea. Why is Paytm Mall not utilized by high manufacturers for presents?

WalMart has a enterprise mannequin of ‘on daily basis low value’. We comply with an analogous technique in funds. Fairly than providing offers in just a few high-end manufacturers, we provide cashback on each transaction whether or not it’s petrol, electrical energy or an iPhone. Our focus isn’t on choose anchor clients and the mannequin is extra inclusive. Additionally, in contrast to e-commerce platforms, we don’t promote our merchandise, quite we’re open to internet hosting all e-commerce platforms on our app.

Some analysts are of the view that funds can’t be a moat…

Fee apps can both come from banks or unbiased service suppliers. It’s now clear that fee app corporations work more durable than banks in offering a buyer expertise. Now if one is utilizing a fee app for transactions, it’s logical that clients will desire these apps the place their cash is. Banks can retailer cash, however they don’t present the identical fee expertise. Paytm has the benefit of storing cash in both the checking account, pockets or by way of a credit score facility. We’ve introduced innovation within the methodology of fee (QR code, cellphone quantity) and added the following degree of comfort (soundbox). Clients can use their fastened deposits to make funds seamlessly. Clients can use Paytm for toll fee on Fastag with out blocking their funds.

So apart from lending, how will Paytm be getting cash?

Every thing on the app past making fee is income producing. Actually utilizing the pockets for funds in organised retail, or funds utilizing Fastag generates income. UPI is like bread and milk in a kirana store, it might not herald revenues however does develop the ecosystem.

Fee gateway Billdesk made a revenue of Rs 270 crore. How a lot did Paytm make within the fee gateway enterprise?

Our income from fee providers to retailers was up 64% to Rs 400 crore. That is pushed by non-UPI fee quantity development in fee gateway and development in units.

The RBI has mentioned {that a} fee financial institution’s transition to a small finance financial institution will be allowed solely after 5 years?

We’re lower than one 12 months away from finishing 5 years (om Might 2022) and are open to exploring the alternatives ought to they come up. Additionally, Paytm Funds Financial institution’s internet price is Rs 400 crore as in opposition to the Rs 300 crore prescribed by the regulation.

The pandemic and subsequent lockdowns gave a push to digital fee and e-commerce. What affect would the easing of restrictions have?

There’s an upside to income from journey, film and occasion ticketing, which had been hit by lockdown in the course of the pandemic. We predict an excellent response from clients because the unlockdown takes place.

How do you count on the market to reply?

Hopefully extra folks available in the market are capable of see our efficiency intimately. We listed in India so that everybody will get a possibility to take part. It is vital that the retail investor will get the entire image. Sure, our losses have elevated 8%, however our revenues have gone up 64% and ebitda has gone up 50%. That’s the full image.

Supply: Times of India