Even just a few years in the past, digital lending was seen as a pathway to profitability for Indian fintech firms. In contrast to digital funds, the preferred sub-segment in fintech by way of enterprise funding, lending had a transparent solution to profitability—the unfold between their value of funding and the rates of interest they cost their clients.

In a research revealed in 2018, the Boston Consulting Group projected that digital lending would account for 48% of all lending by 2023, pushed by altering shopper behaviour, technological advances, beneficial laws and digital improvements. Final yr, in one other report, BCG stated the share of valuation for lending startups will enhance from 13% in 2020-21 to 35% in 2024-25. In keeping with a report by Enterprise Intelligence, 29% of all enterprise funding that went into fintech between 2018-19 and 2022-23 went to lending, subsequent solely to funds.

Nonetheless, previously few quarters, development in digital lending has slowed. In keeping with Face, an affiliation of digital lenders, the sequential development in disbursements by its members fell from 82% within the June 2022 quarter to 23% within the September 2022 quarter to only 2% within the December 2022 quarter.

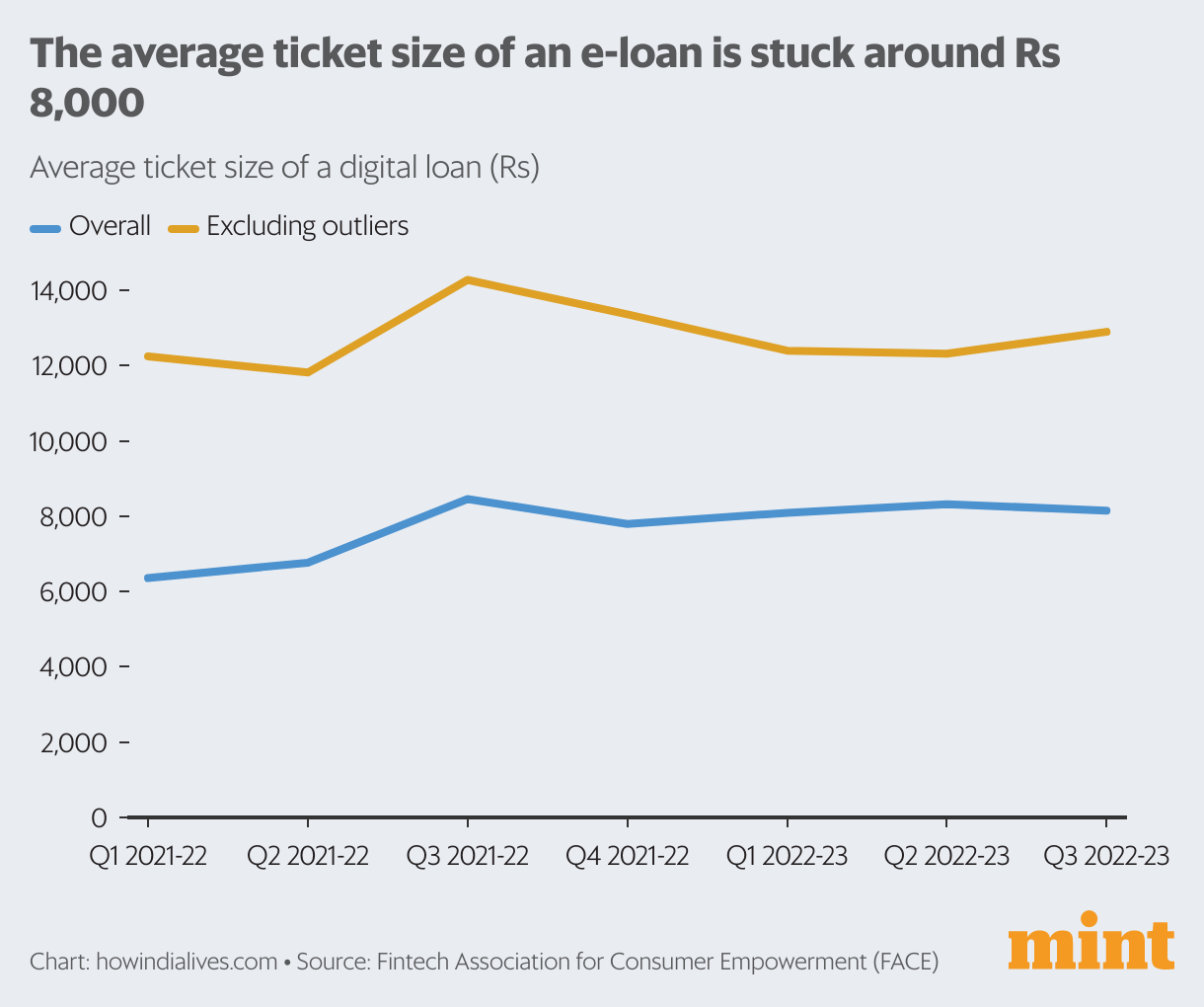

Common mortgage measurement, after rising in 2021-22, has been hovering at ₹8,000-8,300. There are issues that the slowdown in development is perhaps reflective of broader points dealing with the business: larger value of capital amid tightening laws, made worse by the funding winter confronted by startups usually. Opposite to earlier expectations, digital lending startups is perhaps shedding their edge to conventional gamers.

Price Push

Central banks all over the world are rising rates of interest in an try to regulate inflation, after a interval of free financial coverage through the covid-19 pandemic. The Reserve Financial institution of India is not any exception, elevating the important thing repo charge from 4% in Could 2022 to six.5% now. This will increase the price of capital for all lenders. Nonetheless, fintech corporations have historically confronted a better value of capital, partly as a result of, in contrast to conventional banks, they don’t have entry to low-cost deposits.

Digital lenders have additionally been dealing with criticism over larger rates of interest. 58% of debtors took loans from lending apps at an annual rate of interest of over 25%, in line with a survey by Native Circles final yr. Final yr, the Delhi excessive courtroom, after listening to a petition, requested RBI to submit a standing report on excessive rates of interest charged by digital lenders. All these constrain the power of digital lending startups to keep up their web curiosity margins.

Regulatory Squeeze

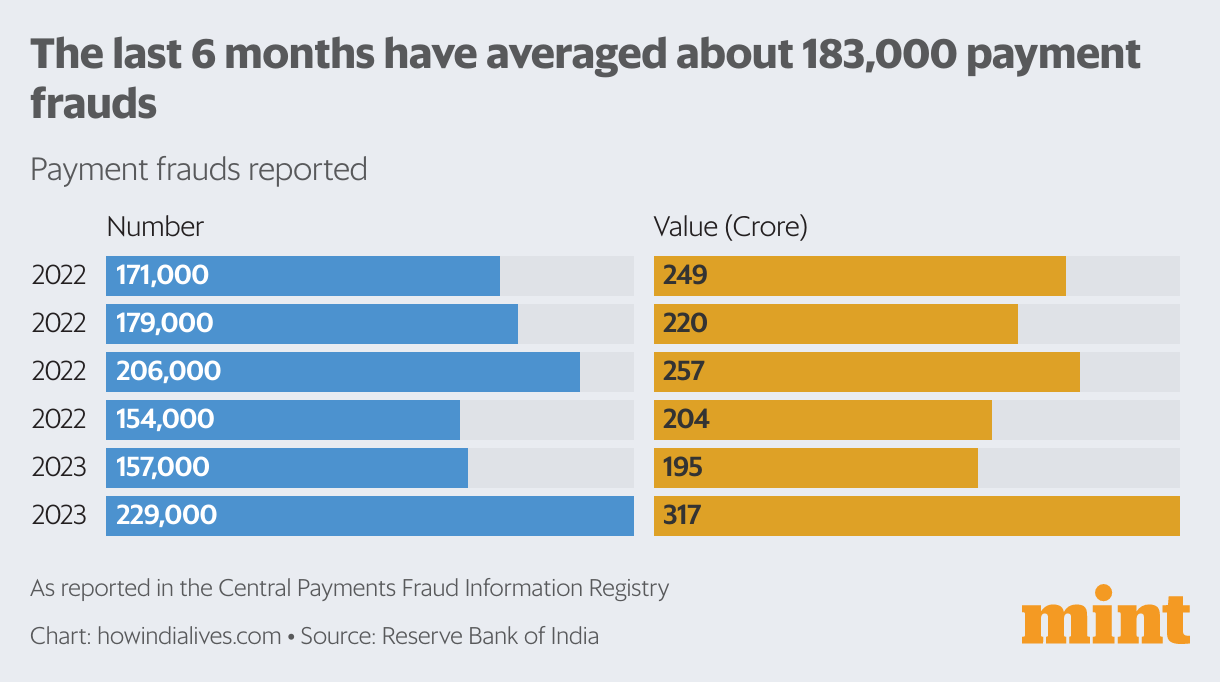

Digital lending apps face much more intense scrutiny over potential frauds. Cost and mortgage frauds are widespread within the monetary sector. In keeping with RBI, within the six-month interval to February, 1.1 million complaints totaling ₹1,442 crore have been reported within the Central Funds Fraud Info Registry by numerous entities, together with scheduled industrial banks. Nonetheless, the scrutiny that digital lending apps have attracted is of a unique order. For instance, final yr, an RBI working group on digital lending recognized 600 unlawful apps working in India. Equally, this February, the Ministry of Electronics and Info Know-how (Meity) banned 94 lending apps attributable to their overseas hyperlinks. It later revoked the ban on a few of these apps and platforms, which additionally highlighted how deficiencies in some platforms can doubtlessly undermine belief of all the section. Tighter laws promise to enhance belief, however they may doubtlessly constrain innovation

Funding Winter

Central banks elevating rates of interest additionally impacted startup funding. Enterprise capital (VC) stream into digital lending startups in India dropped by over 80% to $170 million within the December 2022 quarter, from $887 million within the March 2022 quarter. This drop in funding additionally has implications for startups that raised funding when it was simpler to return by.

The main target has shifted from development to profitability, which is tougher to tug off when the price of funding has additionally risen. Earlier this month, VC agency Bessemer Enterprise Companions revealed a word saying that lending was not engaging as a venture-funded enterprise. “Banks and NBFCs have an unfair benefit on value of capital, India Stack has bridged the expertise hole with the new-age lenders.” It’s a view of 1 VC agency. Digital lending startups will hope it doesn’t turn out to be a extra broadly held view.

www.howindialives.com is a database and search engine for public information.

Obtain The Mint Information App to get Each day Market Updates.

Extra

Much less

Supply: Live Mint