Bharat Electronics Ltd’s sturdy order e-book overshadows the execution hurdles it confronted within the March quarter (This autumn FY22) due to the Russia-Ukraine battle and chip scarcity.

Analysts at JM Monetary Institutional Securities not too long ago met the senior administration of Bharat Electronics the place the latter said that semiconductor scarcity restricted its potential to submit extra income of ₹2,700 crore in FY22. Because the state of affairs eases, the corporate expects to e-book this in FY23. Even so, it goals to attain income progress of solely 15% in FY23. Revenues rose at a lower-than-expected price of 9% year-on-year in FY22 to nearly ₹15,314 crore.

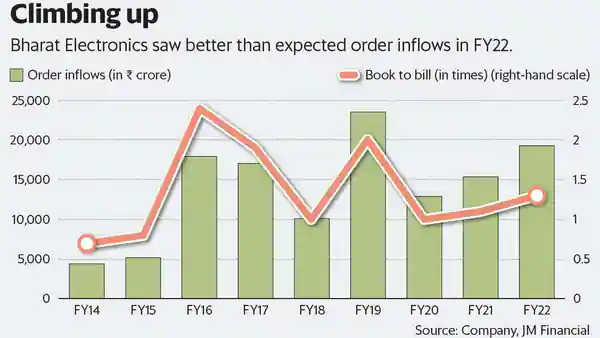

Most of FY23 income is predicted to return from the order e-book of ₹57,570 crore as on FY22-end. This suggests restricted dependence on new orders in FY23. In any case, the corporate expects sturdy order inflows of ₹20,000- ₹22,000 crore in FY23.

The federal government’s transfer to indigenize gadgets corresponding to weapons and programs bodes effectively as it could increase order inflows. Additionally, such measures would result in a drop in materials prices to the extent of 200-300 foundation factors (bps), based on the corporate. One foundation level is 0.01%. It now expects Ebitda (earnings earlier than curiosity, tax, depreciation and amortization) margin in FY23 to be within the vary of 21-23% versus the sooner steerage of 20-22%. In FY22, this measure was 21.6%. “We forecast gross sales and earnings per share CAGR (compound annual progress price) of 16%/19% over FY22-24E led by a sturdy order pipeline, scale up in new companies and elevated indigenization,” stated JM Monetary’s analysts in a report on 14 June.

Nevertheless, the affect on gross margins must be seen because the non-defence combine will increase. Furthermore, the vast majority of the corporate’s order inflows is dependent upon the funds allotted to ministry of defence and this can be a priority. “The current minimize in excise duties, rising subsidies within the agriculture sector, and elevated oil costs already weigh on authorities funds,” stated an analyst requesting anonymity.

In the meantime, Bloomberg knowledge exhibits the inventory is buying and selling at nearly 19 instances estimated earnings for FY24. The corporate’s strong order e-book presents good income visibility. Buyers have taken notice. The shares of the corporate are 7.5% down from the 52-week excessive seen on 19 April, however the inventory has risen by about 14% to date in calendar yr 2022 versus an almost 11% drop within the Nifty500 index. Execution of orders will stay a key monitorable.

Supply: Live Mint